3D Vergetable Cover Net is a three dimensional or in form of honeycombs water permeable polymer or other synthetical material structures, several layers thermal bonded together. They are widely used for fixing soil, grass and small plants roots, also applied in geosynthetics and other construction field. The three dimensional structure retains a layer of top soil and anchors for growing grass roots thus providing a stable surface highly resistant the forces of rain drops and wash away. 3D Vergetable Cover Net is widely used for creating stable vegetation along river, pond banks and slopes to prevent erosion on processes of surfaces. 3D Vegetable Cover Net, Erosion Mat, Landfill Drainage Geonet, Three Dimensional HDPE Geonet Feicheng Lianyi Engineering Plastics Co., Ltd , https://www.lianyigeosynthetics.com

To this end, in the “12th Five-Year Plan†proposal of the tool industry, the development goals of the tool industry during the “Twelfth Five-Year Plan†period are proposed, mainly in the following two aspects:

(1) Significantly increase the market share of domestically produced high-efficiency tools in the high-end manufacturing industry: the market share of the high-end market has increased from the current 10%-15% to more than 30%.

(2) In the provision of “total solutions†for manufacturing cutting operations, the actual pace, that is, in modern manufacturing such as automobile manufacturing, aerospace, energy equipment, etc., selects a number of typical parts production lines, in processing technology and cutting tools. The company implements all-round services and accumulates practical experience in providing “total solutions†for the manufacturing industry.

Therefore, during the "Twelfth Five-Year Plan" period, China's tool industry enterprises are carrying out product structure adjustment and technological innovation around these two specific goals. With the promotion of national science and technology major projects, they have obtained basic and common technologies, tool materials and coating technologies. A number of important achievements have been made to develop a large number of tool products that are urgently needed by key manufacturing companies. Some have broken foreign monopolies, and some provide "integration" in processing technology and cutting tools in modern manufacturing industries such as automobile manufacturing, aerospace, and energy equipment. The solution "has taken the actual pace and accumulated practical experience.

During the "Twelfth Five-Year Plan" period, compared with the sustained rapid development of the previous five-year planning period, the development of the tool industry can be said to be ups and downs, complicated and changeable, and the uncertain factors have greatly increased. Under the new normal, while the demand for low-end tools in the manufacturing industry has fallen sharply, the demand for high-tech modern high-efficiency tools continues to grow steadily, indicating that the demand structure of China's manufacturing industry is undergoing major adjustments. Through on-the-spot investigations of some representative industries, a number of leading tool companies during the “Twelfth Five-Year Plan†period have made great progress in “adjusting structure and promoting transformationâ€. Taking the "three high and one special" high-efficiency tools widely used in modern automobile manufacturing as an example, the investigation at the end of the "Eleventh Five-Year Plan" shows that the localization rate of the tools of the main engine factory (powertrain) is around 10%-15%. At the end of the “Twelfth Five-Year Planâ€, the localization rate was generally 20%-30%. Among them, the localization rate of tools for the main parts and components of self-owned brand automobile engines has reached more than 80%. Progress is obvious. Of course, the proportion of localization of high-end tools is uneven in the development of various sub-fields of the manufacturing industry; within the tool industry, the pace of structural adjustment among enterprises has also shown great differentiation. In general, during the "Twelfth Five-Year Plan" period, under the new situation, members who can achieve strengths and avoid weaknesses, accurately locate, embark on the path of transformation and upgrading that suits their own and achieve remarkable results, the proportion is less than 30%; most enterprises are Efforts have been made in “adjusting the structure and promoting transformationâ€, and progress has been made. It will soon regain its vitality when the macroeconomic situation has eased (such as the acceleration of global manufacturing recovery in 2014 and the role of national micro-stimulation), but it will enter 2015. When the downward pressure on the economy increased, it was once again in difficulty. The main reasons were the ups and downs of the international economic recovery and the lack of domestic innovation and resilience. A few companies were waiting to wait and see the government introduce more stimulus policies to help enterprises tide over the difficulties ( Some of the traditional tool manufacturers owned by the company have experienced a deep decline, and the situation is worrying!). In general, the achievements in the transformation and upgrading of tool enterprises during the “Twelfth Five-Year Plan†period are relatively obvious in the vertical direction. There is still a big gap in the development needs of China’s manufacturing industry from large to strong, and it requires continuous efforts of the whole industry. !

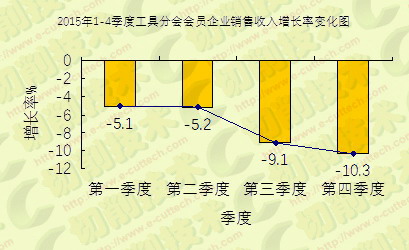

Figure 1 Change in sales revenue growth rate of member clubs in the first quarter of 2015

According to the statistics of the tool club, the total consumption of China's tool market in 2015 decreased by 9.6% to 31.2 billion yuan (see Figure 2), of which domestic tools were 19.6 billion yuan, down 11.3% year-on-year; imported tools were 11.6 billion yuan, down year-on-year. 6.5% (see Figure 3); tool exports were 7.6 billion yuan, down 2.6% year-on-year.

Figure 2 Change in consumption scale of China's tool market in 2005-2015

Figure 3 Change in the scale of China's imported tool consumption from 2005 to 2015

Third, the economic operation of the first three quarters of 2016 has entered the year since 2016. Under the background of the development of the macroeconomic situation in the country, the tool industry is facing greater downward pressure, but the situation of stabilizing and stabilizing is very obvious. Good development.

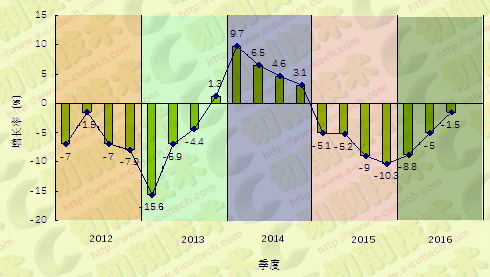

Figure 4 Change in sales growth rate of member companies from the first quarter of 2012 to the third quarter of 2016

As can be seen from Figure 4, this year's sales situation is lower than last year, although the trend is reversed. Last year, it was a deep down month by month. This year, the decline was narrowing month by month, indicating that the market situation is improving. Direction development: In the past few years, under the guidance of the correct policy of “adjusting structure and promoting transformationâ€, industry enterprises have actively adjusted product structure, improved service level, and gradually turned service targets from traditional manufacturing to automobile manufacturing, aerospace, precision molds, In the modern high-end manufacturing fields such as power generation equipment and electronic products, sales revenues that have fallen sharply due to the reduction in demand for traditional low-end standard tools are being compensated for in the growth of high-end tool sales for modern manufacturing services. This is a very encouraging development.

According to the exchanges of foreign counterparts, the sales of imported tools in 2016 also experienced the process of falling from the first half of the year to the second half of the year, but the year-on-year decline was restored from the average of 5% to the same period last year.

2. The average profit level of the tool industry enterprises has increased significantly year-on-year. Although the improvement of the sales situation this year is only recovery, the sales revenue has only recovered to the level of the same period last year, but the good news is that the average sales profit has increased significantly compared with last year. In the first three quarters of this year, 50% of the total profits of the company's statistics increased year-on-year, indicating that the majority of enterprises faced changes in the external market environment. In the process of “adjusting structure and promoting transformationâ€, they also paid attention to continuous improvement of management and saving. Consumption, reducing costs. In particular, no longer blindly pursue the growth of quantity, and generally achieve sales by sales, reflected in economic indicators, and the liquidity occupation and interest expenses have dropped significantly, which has become an important factor in the rebound of the industry average profit this year.

3. Tool exports have double-digit growth year-on-year. In 2016, in response to changes in domestic tool consumption market demand, industry companies have paid more attention to product exports and increased the intensity of expanding the international market. According to the statistics of the tool clubs, the industry in the first three quarters of this year 42% of the enterprises with export products have increased their export products. The export of tool exports in the whole industry has increased by 12.6% compared with the same period of last year. A group of long-term tool export enterprises have strived to improve quality, develop varieties and optimize services. In terms of exporting knives into Europe, the United States and the industrial sector, significant progress has been made (for example, the export of Xiamen Golden Heron has doubled, Dalian Far East has still increased by 64.9% on the higher base of last year, and Zhuzhou Diamond has also maintained export growth). This performance has been achieved without a significant increase in international market demand, indicating that the adaptability and competitiveness of China's tool products to the international market is gradually increasing.

It should be pointed out that this year's industry production and sales situation is steadily improving, reflecting the overall trend of industry development, and does not mean that every enterprise has experienced such positive changes. This year, about 40% of the members of the member companies that have grown against the trend. It can be expected that with the progress of the industry's transformation and development, the proportion of superior enterprises will continue to expand. At the opening meeting of the sixth meeting of the seventh session of the sub-division held in early December, the directors and invited member representatives discussed the hot topics of how to accurately position the characteristics of each enterprise, adjust the product structure, and transform the development mode. , conducted a full conference exchange. The meeting reached a consensus: in the face of the market changes of “significant reduction in total demand and accelerated acceleration of demand structureâ€, the goal of transformation and upgrading of the tool industry is very clear, that is, it is necessary to keep pace with the development of modern manufacturing in China and to improve the production efficiency of manufacturing. To provide more "three high and one special" modern knives and digital precision measuring instruments, to make "innovation" and "service" become an important starting point for enterprise transformation and upgrading, the focus of product structure adjustment is to replace "import" To avoid homogenization competition.

In the process of transformation and upgrading of the whole industry, the industry standard work will demonstrate its importance in the development of modern high-efficiency tools and the traditional standard tool system. We believe that our annual meeting will promote the development and upgrading of industry standardization work, and standardize the industry. Work better for the transformation and upgrading of the tool industry.

Economic operation of the tool industry during the “Twelfth Five-Year Plan†period

Abstract 1. During the “Twelfth Five-Year Plan†period, a brief review of the operation of the tool industry was carried out according to the statistical calculations of the data and tools of the National Bureau of Statistics. In 2010, at the end of the “Eleventh Five-Year Planâ€,

I. Brief review of the operation of the tool industry during the “Twelfth Five-Year Plan†According to the statistics of the National Bureau of Statistics Data and Tools Branch, by 2010, at the end of the “Eleventh Five-Year Planâ€, China’s domestic tool consumption exceeded the highest level in 2008. , reached 33 billion yuan. Although the sales scale of China's tool market has been in the forefront of the world, the domestic tool market share has reached 65%, but the domestic tool products are backward in structure. Most of the domestic tools are traditional high-speed steel standard tools and general-level hard alloys. Standard tools; modern high-efficiency carbide tools that meet the high-end needs of the manufacturing industry, high-performance high-speed steel tools and new super-hard tools account for only about 15%. Looking at the status quo of China's tool industry, by 2010, at the end of the “Eleventh Five-Year Planâ€, although there are more than 700 tool enterprises above China's scale, there are only about 30 companies that can provide modern and efficient tools (the backbone companies in China have control companies). 10, about 20 small and medium-sized outstanding private enterprises). Therefore, from the perspective of the industry as a whole, the main service target of domestically produced knives is domestic low-end manufacturing enterprises, and the high-end market is basically occupied by imported knives.